By Sushmita Solanki

The ambit of Universal Health Coverage

Universal Health Coverage means that all individuals and communities have access to health services they need without suffering financial distress. It encompasses a complete range of essential, quality health services, from health promotion to prevention, treatment, rehabilitation, and palliative care throughout one’s life.

Universal coverage is based on values such as social cohesiveness, the belief in everyone’s right to the best health possible (as stated in the WHO Constitution), or on a “right to health” or “right to fair access to health care,” as stated in many national constitutions. However, from the standpoint of health system performance, UHC, as defined in the World Health Report (WHO, 2010) is ideal since it encompasses both a final goal and intermediate targets with solid linkages to ultimate aims. As a result, even though UHC may never be completely realized, progress toward UHC is crucial for all governments. The goals of enhancing fairness in service usage, service quality, and financial protection, are universally shared.

It is justified from the standpoint of health system performance because it suggests progress toward the goals of health systems: directly in terms of financial security, and implicitly through the intermediate objectives associated with adequate coverage, on the goals of health and responsiveness. To put it differently, it is better to think of UHC as a path rather than an endpoint or a destination. Expansion of health insurance coverage is a vital step and a pathway in India’s effort to achieve Universal Health Coverage (UHC). Low Government expenditure on health i.e; less than 2% of the GDP has constrained the capacity and quality of healthcare services in the public sector. It forces a majority of individuals – about two-thirds – to seek treatment in the costlier private industry. However, low financial protection leads to high out-of-pocket expenditure (OOPE). India’s population is vulnerable to catastrophic spending and impoverishment from expensive trips to hospitals and other health facilities. The devastating effect of healthcare spending is not limited to the poor – it impacts all segments of the population. This situation is not only damaging the health of the Indian people – but it is also a significant impediment to further social development and economic growth. Pre-payment through health insurance emerges as an essential tool for risk-pooling and safeguarding against catastrophic (and often impoverishing) expenditure from health shocks. Finally, pre-paid pooled funds can also improve the efficiency of healthcare provision.

Penetration of Private Health Insurance in India

What matters is not how a particular financing scheme affects its members but how it influences progress towards UHC at the population level. Financing healthcare expenditure via health insurance is gaining significance in developing countries like India. The estimates depict that health insurance is low and not uniform across states and union territories.

India spends roughly 4% of its GDP on healthcare, which includes both private and state spending. However, at 1.2 percent of GDP, public spending is the lowest among the BRICS countries (Brazil, Russia, India, China, and South Africa) (Bansal 2016; MoHFW 2016). Because of the low amount of public spending, over two-thirds of total health expenditure is in the form of out-of-pocket (OOP) expenditures, which account for around 90% of total private expenditure (WHO, 2010). Households are compelled to forego other basic needs, liquidate household assets, and incur debt, due to this excessive OOP spending. According to estimates, roughly 2%–3% of India’s population is forced below the poverty level each year (Van Doorslaer et al. 2007; Garg and Karan 2008), and nearly 500 million people were pushed below the poverty line in 2015, according to the recent World Bank study (WHO and World Bank, 2017).

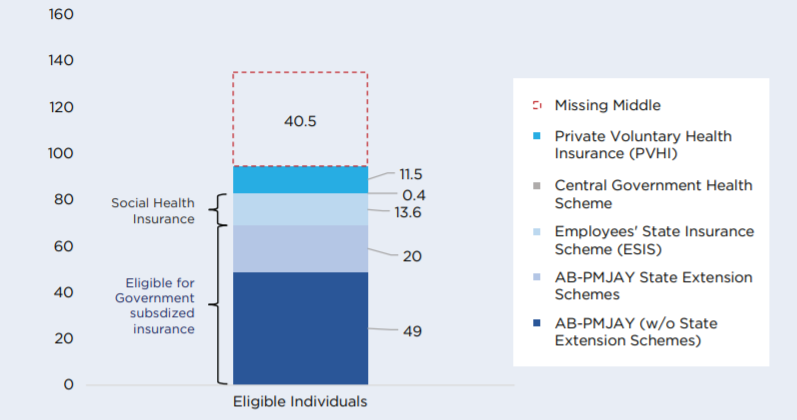

Figure 1: Number of individuals eligible or covered by health insurance scheme type

Source: Niti Aayog report “Health Insurance for India’s Missing Middle.”

Private Voluntary Health Insurance Schemes are contributory and voluntary schemes. These are retail insurance products with coverage of nearly 11.5 crore persons. PVHI is broad of two types — individual/family or group business (excluding Government). The former is targeted towards individuals and families and covers 42 million persons. The latter is targeted towards private enterprises for their employees; these cover 73 million individuals. Group insurance schemes target corporates and private enterprises with higher employee compensation than the Rs 21,000 ceiling under the Employees State Insurance (ESIC). Though the PVHI market had nearly doubled from 61 million in 2013-14 to 115 million in 2018-19, it only covers 9% of the total population. Health insurance is a growing segment of India’s economy. The entire health insurance market – as measured by premium collected – more than doubled from Rs. 20,000 crores in 2014-15 to nearly Rs. 45,000 crores in 2018-19 as per IRDAI’s latest annual report.

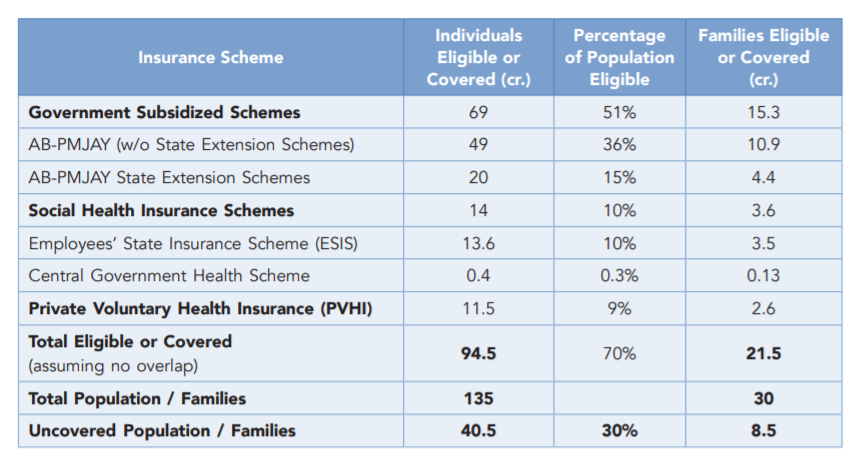

Table 1.1: Number of individuals and families eligible or covered by health insurance scheme type

Source: Niti Aayog report “Health Insurance for India’s Missing Middle.”

Effect of Private Health Insurance on three dimensions of Universal Health Coverage

Health insurance thrives on the fear and uncertainty of the future. The risk of the unexpected or unforeseeable is the fundamental premise motivating individuals to acquire insurance in the “utmost good faith” to protect themselves against future ailments that may jeopardize their health care. In the pandemic, people that were hospitalized that had prior insurance plans had their claims declined or received fewer shares than they were promised. According to a report by Saraswathy, as of 6 February 2021, there were 8,70,000 COVID-19-related claims worth `13,100 crores filed, but the payout had been only `6,650 crores which were insufficient. It’s worth noting that the sum of premiums obtained by insurance firms from individual or family plans was nearly double the amount of reimbursement they provided, indicating profiteering amid a health crisis.

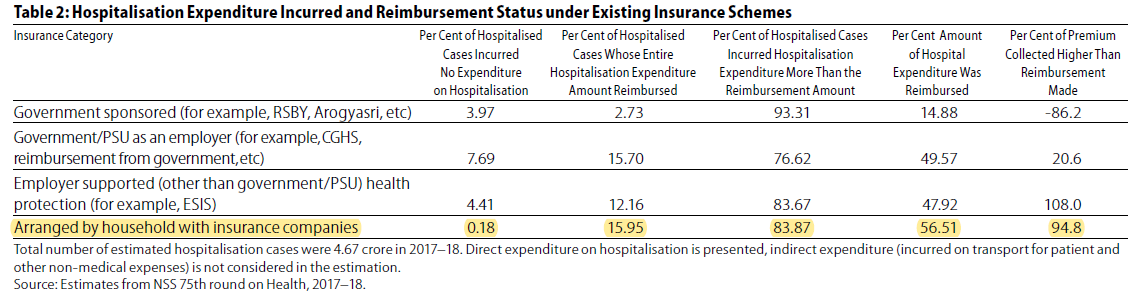

Table 1.2

As per the estimates from the 75th Health Round of the National Sample Survey Office (NSSO) 2017–18, only 56.51 percent of inpatient medical expenses were redeemed through insurance policies pre-arranged at the household level from insurance companies, effectively leaving 43.5 percent to be paid out of pocket, as shown in Table 1.3. The experiences of existing insurance scheme users in securing claims are not very encouraging in India.

In light of COVID 19, in June 2020, The Insurance Regulatory & Development Authority of India instructed all general and health insurers to issue short-term COVID-19 specialized insurance, called Corona Rakshak and Corona Kavach, to individuals and groups, respectively. The Corona Rakshak was voluntary, but it was made mandatory for insurers to provide Corona Kavach. In the year 2020, around 17 firms launched Corona Rakshak products. There was no precise information about the Corona Rakshak renewal; however, 30 Corona Kavach products were available for 2021. On a positive diagnosis of COVID-19, necessitating hospitalization for a minimum continuous duration of 72 hours and 24 hours under Corona Rakshak and Corona Kavach, respectively, a lump sum benefit equivalent to 100 percent of the sum covered (‘50,000 to ‘2,50,000) had to be payable, according to the directive.

Corona Kavach provides coverage for 15 days before hospitalization or residential care treatment, as well as 30 days after release from the hospital or completion of home care treatment. Despite having such coverage, according to multiple news reports, people ended up paying more than 40% of the treatment expenses out of pocket. We may deduce from the above illustrations that PHI has failed to satisfy the three elements of UHC, namely, access to healthcare, coverage, and financial risk.

Critical Challenges in increasing the coverage of Private Health Insurance

- Awareness: A complex product like health insurance has a low uptake due to a lack of knowledge and difficulties comprehending it. The idea of paying for a product that you do not intend to use is counterintuitive. In other words, it is a difficult choice to make ahead of time: to pay for financial insurance against some (uncertain) possibility of future ill-health at the expense of current consumption. Health insurance consumer education, particularly among the middle class, is critical to increasing uptake. Promoting the plan in terms of loss aversion to people who make frequent and costly trips to OPDs can improve the acceptance of the insurance product. However, raising awareness can only be successful if the advantages supplied under the plan are sufficiently appealing compared to those currently accessible in public sector institutions for free or at heavily reduced rates.

- Identification and outreach: On the supply side, this is a significant roadblock. The informal sector employs a large portion of the missing middle, accounting for 80 percent to 90 percent of India’s labor force (PLFS 2018-19 and Report on Employment in the Informal Sector and Conditions of Informal Employment, MoLE, GoI, 2013-14), and there is a lack of a rigorous central repository or other sources for verification and engagement of employee database. As a result, reaching out to potential clients is tough for insurance companies. Insurance firms have either failed to identify and target this population segment or have found it unprofitable to do so. As a consequence, health insurance remains mainly out of reach for the uninsured. Only an extensive and diverse risk pool can ensure the viability of the voluntary contributory health insurance program. To generate demand, a significant push on communication to new consumers is necessary in addition to increased health insurance awareness. To begin, insurers and third-party administrators (TPAs) should try out different incentive schemes to increase enrolment. Incentive clauses, for example, might be included in contracts to incentivize attaining a critical mass of clients within a specific time frame. Second, after obtaining agreement from agricultural families, government databases like the National Food Security Act (NFSA), PMSBY, or (PM-KISAN) can be shared with commercial insurers. Insurers will be able to more easily identify and reach out to potential clients using such databases.

- Affordability: The middle class highly price sensitive. To ensure great deals and high demand, it will be necessary to reduce the product’s expenses whenever possible. There are two main areas where add-on costs, or fees beyond the actuarially fair premium, might be reduced to minimize the product’s cost.

- Distribution Costs: Group targeting lowers the average logistic costs per policy compared to individual targeting. By focusing more on digital platforms for health insurance sales, commission expenses will be reduced. Post offices and regional rural banks are examples of government assets that can be used as distribution networks to expand insurance coverage without incurring high costs.

- Operational costs: The operational expenses for standalone health insurers are around 25% of the total premium collected, driven by high claims processing costs. Increasing the use of analytics, standardized formats for more effortless data flow and digital tools to improve efficiency and generate economies of scale through higher volumes can reduce operational costs.

- Adverse Selection and Preferred Selection: In health Insurance, Adverse selection occurs when the number of high-risk, sick policyholders surpasses the number of healthy policyholders. Therefore private health insurers would want a higher number of healthy policyholders compared to sick policyholders. Implementing measures to avoid adverse selection are likely to lead to preferred choice or cream-skimming, which is inherently incompatible with India’s goal of achieving Universal Health Coverage. Group enrollment is the most effective way to increase the number of policyholders in the risk pool. It also has the advantage of providing greater bargaining power to individuals aggregated through groups against insurers. Greater bargaining power can help address grievances and improve the efficiency of health insurers.

Conclusion

Private Health Insurance’s role in achieving UHC in India has been limited so far and the challenges looming around PHI have failed to fulfill the three elements of UHC, namely, access to healthcare, coverage, and financial risk. The policymakers need to acknowledge the role of private health insurance in healthcare systems and regulate it effectively to achieve shared goals of universal coverage and equity. To encourage fair access to PHI, policy analysts should propose strong government rules against voluntary enrolling and risk-pricing of PHI.

Sushmita Solanki is a second-year Masters’s Student at the Jindal School of Government and Public Policy. Her research interest areas are Urban housing, Health system financing, and Monitoring & evaluation.

Image credits – Forbes