Stalin would turn in his grave if he read the title of this piece. To be fair, it’s not just him, but many others who have been sceptical of privatisation of economies and an equal many in favour of it – making it an interesting debate. In the contemporary world, increasing globalisation has brought the economies closer – increasingly allowing free and open access into each other. This trend has led the literati to debate over the pros and cons of privatisation and its role in economic growth and development. This piece concerns itself with understanding the role of privatisation in causing economic growth (in terms of annual growth in GDP). It does so by discussing the qualitative arguments both, in favour and against privatisation followed by briefly looking over consequences of economic liberalisation in the past in India, China and Thailand. Further, this piece will look at privatisation through the lens of certain economic theories and growth models. Finally, it will wrap-up by discussing some other important factors influencing the relationship between privatisation and economic growth led by a summary conclusion.

This piece flirts with arguments on both sides of the debate around privatisation. However, before diving straight into them, it is imperative to understand the meaning of ‘privatisation’ of the economy. It is the transfer in ownership of enterprises, firms and property from the public (government) to private players. Privatisation implies economic liberalisation in almost all cases. Economic liberalisation is the reduction of government regulation and restrictions, allowing the larger participation of private players. This process significantly cuts down on ‘red-tapism’, allowing the firms and enterprises to work efficiently. It reduces the deadweight loss and fosters optimal use of resources. It helps in the establishment of a free market where price competition often drives the prices down, subject to the demand and supply patterns. The profits obtained in the market incentivises firms to produce better quality goods and services. Moreover, economic liberalisation enables foreign trade by following a ‘Deregulation, Liberalisation, Privatisation and Globalisation’ (DLPG) model. This enables the economy to access newer commodities at possibly cheaper prices. Privatisation also increases the ease of doing business, attracting more foreign direct investments (FDIs). The government also raises revenues through the sale of their assets which could be used to cover fiscal deficits or spent in social welfare schemes.

On the flip side, privatisation of some sectors could lead to the emergence of natural monopolies instead of competitive markets. This happens when the market good or service requires huge fixed cost investment at the start and the firm enjoys continued ‘economies of scale’ for a long time as it increases supply because the variable cost is minimal. For example, it takes a one-time higher cost to build telephone lines in an area, but as and when more and more connections are sought, the average fixed cost of the firm reduces enabling economies of scale. Such monopolies can be exploitative and charge higher prices. Moreover, monopolies and cartels are also very difficult to regulate. The reduction in regulations and restrictions over markets and sectors also generates a fear of losing power and control in the government, thus making it unwilling to privatise to keep its power intact. Additionally, private sector is more profit oriented and cares less for the society. Hence, privatisation of certain public services such as healthcare, education and transport may generate more accounting revenues, at the cost of high social losses. The idea of privatisation and competition also widens the wealth inequality within and outside the economy. Therefore, privatisation has significant risks too which need to be mitigated.

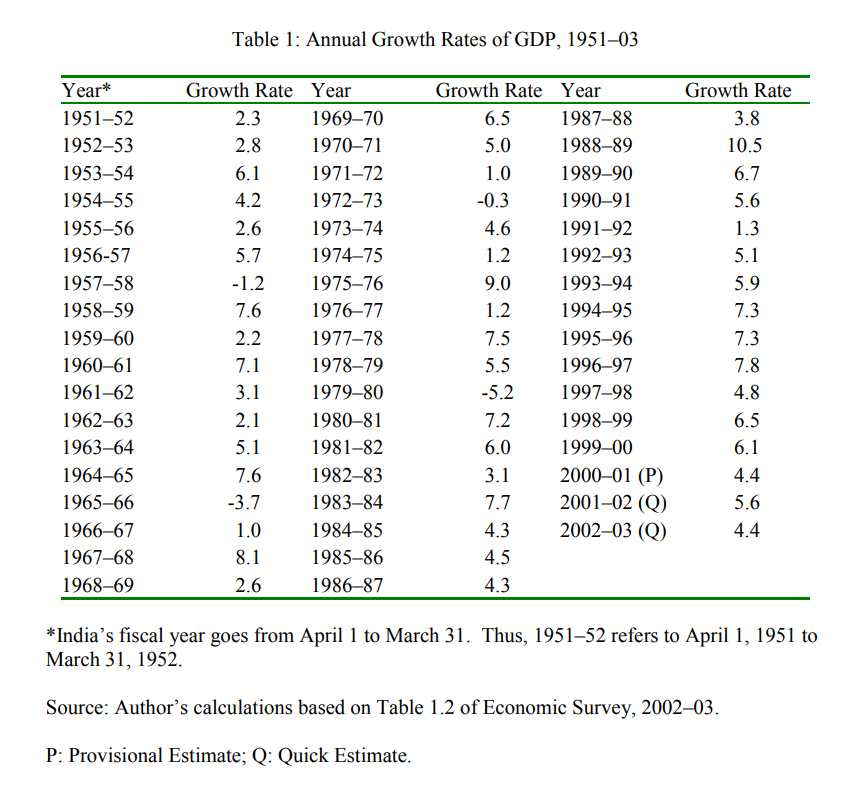

Crunching numbers for certain economies such as India, China and Thailand would enable a more formal analysis of privatisation’s role in driving economic growth. India’s reform and economic liberalisation in the early 1990s included reduction of import tariffs and deregulation of markets leading to increased privatisation and a reduction in taxes. It is clear from the table below that as a result of these reforms, India’s annual GDP started growing at a significant and sustainable rate, after being quite volatile earlier. FDI into India too saw a 316.9% rise from 1992 to 2005. This clearly indicates a positive effect of privatisation on the Indian economy post reforms.

Table 1 [Source: IMF Working Paper WP/04/43, March 2004]

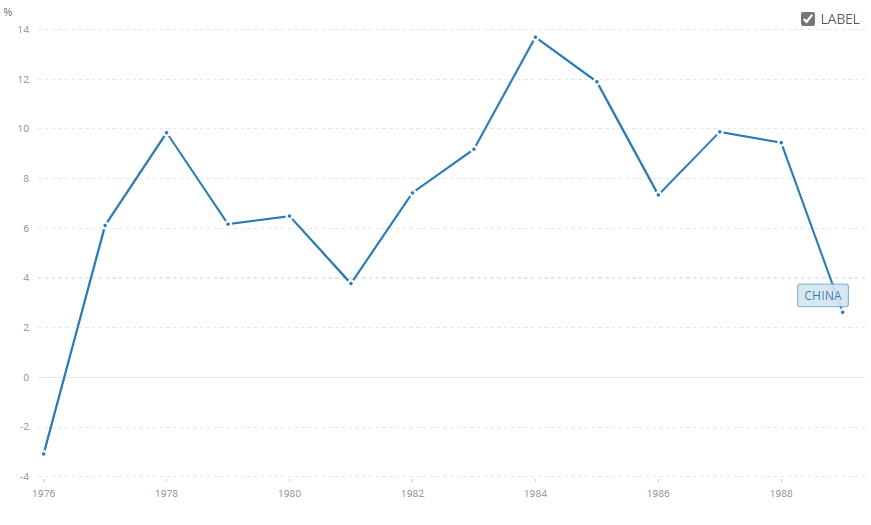

Similarly, during gǎi gé kāi fàng or the ‘reform and opening up’ of China under Deng Xiaoping, China adopted an open-door policy, allowing international firms to tap into its large markets and carry out trade and investments. China’s state-led market system was a success and got China a seat at the ‘adult’s table’, making it an important stakeholder in the global economy. The graph below shows China’s tremendous growth, which it sustained throughout the Deng-era. It also paved China’s way to overtake Japan to become the world’s second biggest economy in 2011.

Figure 1 [Source: World Bank Dataset]

The counter attacks to privatisation can be mounted on the failures of the Thai economy which triggered the 1997 Asian Financial Crisis. In 1997, when the Thai Central Bank removed its currency peg against the US Dollar, completing its liberalisation process, the Baht plummeted – triggering the crises. It is important to note here that in the early phases of Thai economic liberalisation (mid 1980s onwards), the economy performed remarkably well, with a double-digit growth and the tag of the fastest growing economy in the world in late 1980s. However, it was the poor policy implementation and crony capitalism which accompanied Thai economic liberalisation that hollowed the economy, draining foreign reserves, leading to the 1997 crisis. The above examples make it increasingly clear that privatisation leads to significant positive changes required for economic growth if implemented with caution.

Now, going back to the textbooks to see how privatisation fits into some of the classic economic growth models can prove to be a fruitful exercise. The Solow Model talks about capital accumulation in the economy, it highlights the importance of capital investments for developing economies to achieve faster growth. Privatisation enables fresh capital investments into enterprises which were earlier state-owned, thus creating more jobs and increasing the productive capacity of the economy. Plus, acquisition of labour augmenting technology through faster, private channels can improve the total factor productivity in the Solow economy leading to higher growth in the short run. Moreover, privatisation encourages stronger patent protection laws which incentivises firms to carry out Research and Development (R&D). Hence, privatisation of public firms in the Schumpeterian growth model too shows a positive impact on economic growth.

Nevertheless, to reiterate, privatisation is a means to an end and not just an end in itself. In simpler words, there are other aspects too which complement privatisation in making a positive impact on the economic growth of a country. These factors differ from economy to economy. As illustrated through the example of Thailand and China, privatisation must be checked in order to induce higher positive economic growth and prevent things from going south. Leadership and the regime type are leading factors which overlook the extent of privatisation of the economy. A strong leader in a tighter regime can better regulate the economy as opposed to a weak one in a democratic republic. China is one of the best examples of a state-run market economy where the firms participate in free market capitalism and behave like private entities despite being Chinese state-owned-enterprises (SOEs). Moreover, the country must have enough state-capacity to efficiently regulate the markets without too much interference. This draws attention to the scope of public-private partnerships (PPPs) in boosting economic growth. Regulated privatisation of public sector undertakings (PSUs) creates a win-win situation for everyone as it increases efficiency of the firms and at the same time checks private interests of the players. Therefore, privatisation alone cannot be an answer to achieve high economic growth – or simply, an end in itself.

In conclusion, there are a nexus of opinions around the viability of privatisation of economies. While neither extreme on this spectrum of opinions can be termed as a clear winner, the sense is to strike a favourable balance between privatisation and centralisation (or nationalisation) of the economy. In the words of an economist, an “equilibrium needs to be achieved and maintained” between the two in the long run. Simply privatising the economy is like making a king without wisdom. And it would be a better option to send everyone to the Soviet ‘Gulags’ before fully nationalising the economy – because that’s possibly the only way the government can know everything and make a perfect central plan for allocating resources and setting prices. Therefore, on the outset yes, privatisation is a boon that causes economies to boom. However, the method of implementation of such a privatisation campaign is also equally significant in determining its success or failure. All these factors if properly balanced should put economies on a sustainable growth path in the long run*.

*All privatisation exercises and policies are subject to market risks. One must read and implement all the scheme related documents carefully.

Deepanshu Singal is an undergraduate student at Ashoka University with a keen interest in Economics and International Relations.