Abstract

The world observed the deadliest financial crisis since the great depression of the 1930s in 2008. The signs of a financial crisis started becoming visible in the mid-2007 and early 2008 by the demise of stock markets, the failures of big financial institutions in the United States and parts of Europe. Given that banks play a key role in our modern market system due to globalization, the crisis quickly swelled through the whole real economy, which turned a financial crisis of the United States into a global economic crisis. The crisis affected many regions of the world in different ways due to their diverse interaction with the United States. In this paper, I examined the effect of the crisis in Africa more precisely Ghana and South Africa. The impact was analyzed with regards to the performance of Gross Domestic Product, Balance of Payments, Fiscal Deficits, Net Investment Levels, Inflation indices and the Trade statistics of the both countries.

1. The Great Recession of 2007

1.1 Background to the Crisis

The years preceding 2007 are often been referred to by economists as the years of the Great Moderation, since these were years advanced economies witnessed stable growth rate, and vast macroeconomic stability. In 2001 the US Fed lowered the interest (The Fed fund rate) rate from 6.5% to a drooling 1.75% (Singh 2011). Thus creating a flood of liquidity in the economy. Bankers and reckless borrowers who didn’t have a permanent income or job came seeking credits due to the overflowing of cheap money. These so-called subprime borrowers came for these loans with the minds of achieving their dreams of owning a home. So, as subprime borrowers increased, so did the prices of homes. This new development made Investment in questionable subprime mortgages seem like a new gold mine.

In 2003 the Fed brought the interest rate down to 1%, thus leading to bankers repackaging mortgages into Collateral Debt Obligations (CDOs) and selling them off. Subsequently leading to the development of a large subordinate market for the distribution of subprime loans. And then the Security Exchange commission of the US went on minimizing the Net Capital Requirement of the five big investment banks in 2004. Thus making these investment banks to Leverage 30 or 40 times their original investments.

1.2 The Crisis

As of June 2004, the Fed started immensely raising interest rates so much that by June 2006 interest rates had peaked 5.25% (IMF 2009). This vastly increased in interest rates led to the start of borrowers defaulting on their loans, causing a bad start of the year 2007 with so many subprime lenders claiming bankruptcy. According to Singh (Singh 2011), hedge funds and some financial firms held more than 1 trillion in securities that were backed by these failing subprime mortgages, making the situation alarming enough to start a global financial crisis if more and more borrowers kept defaulting.

August 2007 came with the clarity that the subprime crisis could not be solved single handed by the US financial markets, and soon the crisis started spreading beyond the borders of the US. Then came the freezing of the inter-bank markets, due to the speculations among other banks. The Fed came into the situation by the slashing of the Fed funds rate as well as the discount rate in an effort to solve the problem, but the worst kept happening. The worst started by the filing of bankruptcy by Lehman Brothers, followed by collapsing of Indymac bank, the acquisition of Bear Stearns by JP Morgan Chase, the selling of Merrill Lynch to Bank of America, and the US Federal government controlling of Fannie Mae and Freddie Mac.

By October 2008, the cross border spillover had deepened in many regions of the world due to inter-linkage of markets and financial institutions with the high correlation of risks. During which time the US Fed reduced the funds and discount rates to 1% and 1.75%. Bigger economies Central Banks like China, England, Canada, Switzerland, Sweden, and the European Central bank took measures to help the global economy from further crashing by cutting down their rates. But the cutting down of rates alone was insufficient to halt such extensive global financial collapse.

2 The Impact of the Crisis on Africa

2.1 Africa Before the Crisis

Granted that Africa is indeed a diverse region and that, not necessarily all economies have coped well. But prior to the 2007 recession, African economies were generally flourishing, they grew at an average of approximately 6%, inflation collapsed into a single digit level below 5%. This was before the food and fuel price shock of 2008 (IMF 2009). This positive growth was attributed to the favorability of the external environment, strong macroeconomic policies, the rise in commodity prices from 2002-2007, and the massive inflows of grant/AIDS and debt reliefs from the international community.

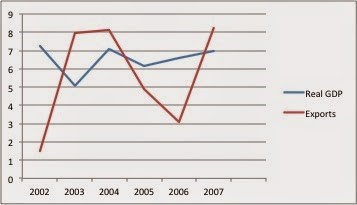

Figure 1. SSA GDP and Exports growth in percentage before the Crisis

Source: IMF data, Author’s accumulation

The graph portrays that the region experienced economic growth at an average of 6.5% per year between 2002 and 2007. The increase in the demand for African primary commodities such as natural resources, particularly oil and minerals was a key drive to the growth of the continent between these periods. This excess demand was encouraged by the growth in industrialized countries and the rise of emerging market economies like China and India. Granted that African growth during that period was driven by a commodity boom, but many other factors such as, increase in FDI, Net private capital flow, portfolio flows, remittances, were anticipated to have expanded between the years. (UNCTAD 2009) In many other African countries, there was an increase in productivity and domestic demand in terms of telecommunications, as the use of mobile phone and internet services grew from 2002-2008. All these trends were aided by enhanced economic governance, fiscal restraint, efficient banking policies, International debt relief programs, and the decline in the number of civil war and insurgences made the continent quite striking for foreign investments.

2.2 Impact of the Crisis on Africa

The recession that started in the US financial markets was a bit slower in affecting African economies, but it gradually did. Right after the fuel and food price shock of 2008, the hard sustained economic gains that Africa had managed to sustain over the years were at risk. Just as in other parts of the world, Africa started experiencing the waves of the financial crisis in 2009. The continent saw a great decrease in the demand of its export, decrease in commodity prices, and the flow of remittances to the continent also started declining. As the situation reached its height, international trade got more costly, foreign direct investors got frightened leading to a fall in FDI, and a tighter international investor and credit risk aversion led to the reversal of portfolio flows. Even fragile states like Liberia, Guinea-Bissau and Burundi whose social and political situation at the time were vulnerable, felt the impact of the crisis due to their dependence on concessional financing. (Bourdin 2009)

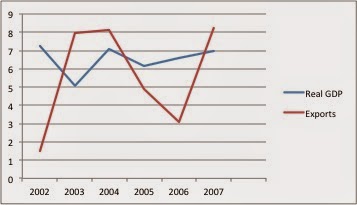

Figure 2. Percentage of SSA Real GDP, Exports, Imports and Current Account Balance

Granting that Africa is the least assimilated region in the world in terms of global trade, yet it was unable to drift away from the effect of the global economic crisis. Despite the continent’s low contribution of approximately 2% to global trade, the majority of its economies depend on the export of their primary commodities for survival. Figure 2 shows a decline from 5.4% in 2008 to 1.3% in 2009 in the total real GDP of South Sahara Africa. Imports, which the continent depends on heavily due to their poor production and manufacturing activities, fell from 8% in 2008 to -4% in 2009 due to the decline in global productions. Due to the continent exposure to industrialized economies, there was a decrease in the demand for African exports leading to exports falling from 8% in 2007 to -0.071% in 2008, and -5.6% in 2009.

The IMF data indicates a general fall in Africa’s economic growth by nearly4%percentage in 2009.The mixture of poor export demand, the decline in private capital flows, worse commodity prices, decrease in remittances, the cutting down in tourism revenues, and fragile government revenues were all reasons that the continent economic growth fell by close to four percentage in 2009. The continent emerging markets or middle income countries that were more assimilated into the global markets were the hardest hit: with growth slipping by about 4.5% in 2009.But in the normal course of events, disparities in economic growth across sub-Saharan Africa are intensely connected with eccentric shocks which were also a reason for the fall in the continent growth. What started with the decline of commodity prices and in some countries affecting the wages of the workforce and even farmers, quickly led to an exit for a total economic collapse and the intensification of the class struggle.

1.3 Why Ghana and South Africa?

I chose Ghana and South Africa because they are both growing economies and emerging markets in Africa. And these economies with financially developed markets were the first to feel the effects of the global financial crisis because they were more assimilated into the global financial market by the connection of capital flows, exchange rates and stock market investors. Given that the first four economies that were hit by the crisis in Africa are; Nigeria, South Africa, Ghana and Kenya, which led to capital flow reversals, a fall in their equity markets, and exchange rate compression, I decided to analyze the Ghanaian economy being from the west, and the South African economy being from the South.

2 Ghana and the Global Financial Crisis

2.1 Trends before the Crisis

There have been a lot of changes in the Ghanaian economy since their independence from the British in 1957. Their economy has gone through so many changes ranging from the poor economic performance from the 1980s that was marked by the coup and lack of market principles in the National economic policy. For the most fact, before the economy started enjoying a period of strong economic growth, they struggled with the issues of low productivity, high interest rates, high and volatile prices, and high interest rates thus leading to a very abnormal growth during those years. These issues lead to many difficulties such as: limited access to International Credit, reduction in foreign direct investment, declining exchange rate and International trade.

The country came back on the track of unprecedented economic growth in the early 1990s, when they took up the multi-party, the neo-liberal project of the IMF and World Bank, and constitutional rule. This return was marked by an increase in the prices of the Ghanaian traditional products (Cocoa and Gold) compiled with a series of market reforms which enable the environment for the growth of the private sector. With the improvements in both the microeconomics and the political conditions, the country has been standing firm on the grounds of a solid economic performance over the past years.

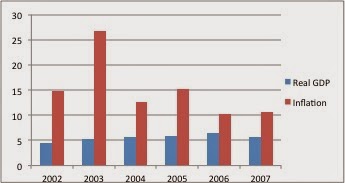

Figure 3. Ghana growth measure by the percentage change and real GDP and Inflation

Source: IMF data, Author’s accumulation

The World Bank data show a growth rate of about 5% per year in the Ghanaian economy over the last 20 years. Within the last few years, the country has been pursuing a more outward trade policy that recognizes export as a key engine for economic growth and prosperity. In figure 3, we see that the period after 2003 was a very spectacular one with a GDP growth rate averaging approximately 5.9% from 2003 to 2007. The proper implementation of macroeconomics policies lead to inflation staying below an average of 15% throughout these years of boom.

The government of Ghana’s principal objective from 2000 was to reduce its domestic debts and stabilize the balance in terms of GDP performance. This objective was realized from 2001-2005 as gradual improvement was seen in the overall performance of the budget balance. But as for fiscal deficits, it was very low due to the new measure of improvement in revenue expansion, and economic expansion.

But with all the improved growth level in the Ghanaian economy, the Current Account balance did speak an actual different story. Figure 4 indicates a current account deficit that kept growing from 2002 to 2007. An economy that is being run on a current account deficit is due to the increase in the value of imports of goods, investment, services, than that of the value of exports. It is sometimes referred to as a trade deficit.

Figure 4. Inflow of FDI as percentage of GDP and C/A balance as percentage of GDP

Source: IMF & ITC data, Author’s accumulation

And this was the case of Ghana during these years, Ackah et al, in their 2009 paper reveal that during 2003-2007 imports increased from $3232.8 million to $8073.57 million. While exports increase just from $2562.4 million in 2003 to $4194.7 million in 2007. (Ackah et al, 2009) But the issue of low export during these years cannot only be attributed to the economy huge dependence on primary commodities. But I can argue that it was attributed to the economy’s heavy dependence on a constricted range of primary commodities without diversification, just like other African economies. I argue this because; Ghana primary commodity in International trade that constitutes approximately 60% of its exports is largely Cocoa and gold. See Figure 5 below.

Figure 5. Ghana Trade Statistics, Imports and Exports as a percentage of GDP over the years

Source: World’s Bank data, Author’s accumulation

3.2 The Impact of the Crisis

Due to the country’s past 25 years of aggressive exports led industrialization, and their enactment of the IMF and World Bank neoliberal policies, they became significantly integrated into the global economy in terms of international trade. So they were not spared from the external shocks of the crisis. Figure 5 shows an increase in Inflation from in 2007 to 16.5% in 2008. This increase can be attributed on account of the external shocks and the strong domestic demand. Just after a brief fall, to single-digits in 2006, inflation galloped in 2007–2008, which reflected the impact of the global food and fuel price shocks, marking the beginning of the global financial crisis late 2008. But the graph indicates that by January-May 2009, inflation did stabilized a bit by 20% percent that is it dropped from 16.5% in 2008 to 14.5% in 2009.

The graph also shows the shifts in the flow of FDI in the economy from 2008-2010. FDI plays a key role in the Ghanaian economy, by means of capital flows as well as employment generation. The decrease in FDI was due to the tension on global capital, exerted by the crisis. This led to a fall in FDI from 9.5% in 2008 to 9.1% in 2009 and it further fell to 7.9% in 2010 (percentage of GDP). The fall in FDI can also be related to that of the decrease in aid/grants and remittances. As many of the industrialized nations that grant aids were pressed by the crisis, the number of aid flow into the economy rapidly decreased from 2007-2009. The crisis also had an impact on exchange rates. The Ghanaian Cedi started depreciating against all other major currencies as of mid-2008.

As the global financial crisis brought a fall in the prices of commodities due to the fall in demand by international companies, the exports of concerned countries began falling. The bank of Ghana reported a fall in the price of the country’s main export which is gold in 2009. The price fell from $965.90 in 2008 to $803.91 in 2009. Gold wasn’t the only export that was affected; exports such as cocoa and other commodity prices as well started declining during the same period. While there were continuous poor performance of exports during that period, Imports on the other hand was increasing due to the export led strategy that made it to produce what was not consumable and consume what was not produced in the economy. See Figure 5.

4 Impact of the Crisis on South Africa

4.1 Trends before the Crisis

South Africa has been Africa’s wealthiest major economy for years, (until recently Nigeria took over) has been a key player in the role of emerging market economies that have helped transform the global economy over the years. The South African growth trends started by their political transmission from the Apartheid regime to the most peaceful political regime in Africa since early 1990s. An intense reformation of the economy did bear a successful fruit in the form of macro-economic stability, flourishing exports and improvement in productivity in capital and labor. This transmission came along with vibrant economic growth that was sustained for almost a decade. The growth was due to the country’s record of a sustained macroeconomic farsightedness that was added to a supportive global environment. The country sustained a GDP growth at a stable pace until the global financial crisis of 2008 and 2009. The sustained GDP growth was also accompanied by the improvement in fiscal balances, leading to the decrease in the government gross debts. Due to the sound policies implemented, the collection of revenue quadrupled and the number of taxpayers increased fivefold between 1996 and 2007. (World Bank)

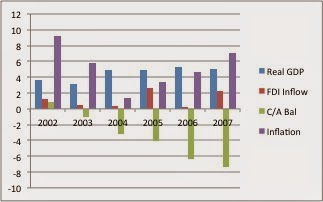

Figure 6. Real GDP (annual % change), FDI Inflow (% of GDP), C/A balance (% of GDP) and Inflation (Annual % change)

Source: IMF & ITC data, Author’s accumulation

Figure 6 indicates the growth trend in South Africa from 2002 to 2007. As shown in Figure 6, South Africa’s real GDP rose by 3.6% in 2002, 3.1% in 2003, 4.8% in 2004, 4.9% in 2005, 5.3% in 2006, which has been cited as the highest 1981 and 5% in 2007. This growth can be attributed to the effectiveness of the bold macroeconomic reforms that have enhanced competitiveness, employment creation and opening South Africa to the multilateral trading system. The country saw its inflation rate going down from 5.8% in 2003 to 1.3% in 2004 but peak again in 2005 to 3.3% which was due to the primary increase in food prices. All these trends were driven by household consumption, private and public fixed investment on the demand side, financial and business services, construction, and wholesale years and retail trade on the supply side.

Figure 7. South Africa Imports and Exports as a percentage of GDP

Source: World’s Bank data, Author’s accumulation

Source: World’s Bank data, Author’s accumulation

After the country’s integration into the global economy, their trading statistics were subjected to enormous changes as Figure 7 rightly portrays. Exports and Imports of South Africa started an actual boom from 2004 to 2008 given that exports rose by 26% in 2004, 27% in 2005, 30% in 2006, 31% in 2007 and 36% in 2008. Imports on the other hand, rose by 7% in 2004, 28% in 2005, 32% in 2006, 34% in 2007 and 30% in 2008. The change in the country’s volume of trade can be ascribed to those reforms that were mainly concerned with at achieving greater economic stability and liberalization. These reforms increased the country’s productivity, favoring trade, and foreign capital flows as never before in the economy.

4.2 Impact of the Crisis on South Africa

The crisis made a severe impact on the South African economy, given that the economy suffered its first recession in 2008/2009 since 17years of economic growth and development. The year 2009 was marked as the largest slowdown in the South African economy, and its impact was even larger than that experienced by some industrialized and emerging economies. The financial crisis was said to have been transmitted into the economy primarily via the financial markets, tightening of bank lending standards and trade linkages due to their integration into the world economy. In South Africa, the financial sector experienced a failure of asset prices, intense increases in the cost of capital along with a severe contraction in loaning. Millions became jobless in 2009 as the result of the crisis. Besides the increase in unemployment, the effect of the crisis was also seen through the increase in consumer demand and consumer credit, the fall of imports and exports, and the sad story of net financial inflows turning into net financial outflow thus resulting in share prices dropping.

Figure 8. Real GDP (annual % change), FDI Inflow (% of GDP), C/A balance (% of GDP) and Inflation (Annual % change)

Source: IMF & ITC data, Author’s accumulation

Figure 8, shows the impact of the crisis on the economy from 2008 to 2010. Real GDP was seen to drop from 3% in 2008 to -2.1% in 2009. The fall in the real GDP in 2009 was a bit narrower as compared to other emerging markets. The fall was quite lower because of the South African economy did not experience any major bank failures or bankruptcy, and the OECD proclaimed this declined to be counterbalanced by the strong growth in the construction industry and cheap oil prices during that period. (OECD 2010) The graph also shows the impact of the crisis on the inflow of FDI in the economy. FDI fell from 3.6% in 2008 to 2.7% in 2009 because of the decrease in the level of confidence of investors. This decrease in the level of confidence of investors led to foreign portfolio investment flows to other emerging countries to be reversed. Additionally the impact of an unstable global capital market and a very poor investment or banking environment placed a downward pressure on the volumes of business and also had a negative effected on fee income. So investment income further dropped due to the poor performance of the global equity markets. Subsequently, the current account balance indicates a decrease in the trade deficit from -7.4% in 2008 to -4.9% in 2009. Inflation, on the other hand, as portray by the chart, fell from 11.5 in 2008 to 7.1 in 2009.

Just as international trade jumped during the global crisis, South African exports of goods (see Figure 7) and services fell sharply as a result. According to Kershoff (2009:8-9), South Africa was hit really hard by the drop in the international demand for vehicles and non-food commodities (industrial raw materials) mainly because these items dominate the country’s exports. Figure 7 shows a fall in exports from 36% in 2008 to 27% in 2009, and imports also fell from 39% in 2008 to 28 in 2009.

Another significant impact on the South African economy was the increased in the rate of Unemployment. The country had previously been suffering from the issue of unemployment and this crisis, unemployment only added up and intensified the existing regional economic inequalities. In mid-2009, South Africa labor force statistics reveals that in 7 of the 9 provinces the unemployment rate had exceeded the national rate of 24.3%, making it the highest in South Africa poorest provinces with a large rural population.

5 Conclusion

Even with Africa’s low integration in the global economy, it was hit hard by the global economic crisis. The continent economic growth went from 5.2 percent in 2008 to 1.6 percent in 2009. Luckily, Africa responded by upholding those good policies that had brought some level of growth in the past, and they continent started recovering in 2010. Notwithstanding, with all the challenges facing the continent, ranging from an enormous infrastructure deficit, weak initial conditions for the 2015 Millennium Development Goals, low agricultural productivity, and very poor governance, Africa’s performance has recently given us cause for optimism.

The 2008 financial crisis was more global than any other period of financial turmoil since the great depression. The degree and severity of the crisis echoed a combination of several factors, some of which are common to previous crises and others are new. In previous financial havoc, the pre-crisis period, was mainly considered by the surging asset prices proving unsustainable, an extended credit expansion that led to the increase in debt, marked by the beginning of new types of financial instruments and the failure of regulators to keep them up.

The slowdown in economic activity that came as a result of the great recession of 2009, left Ghana and South Africa under immense pressure to build their economy back to its pre-crisis level. Many Corporations were affected directly through higher financing costs, as well as secondarily that is through the impact of the crisis on their customers and, their balance sheets. Exports were under pressure due to the decline in world trade, and many jobs were lost in some industries, and in other industries the pressure on wages combined with the costs of production remained high. Even though all financial crises has similarities with previous crises (Great depression, amongst others) in some features, but the effects or the impact of the global financial crisis of 2009 remains the worst ever experienced since the great depression and therefore it remains significantly different.

Faith L. Morlu is a Masters student at Jindal School of International Affairs

References

- Ackah, Godfred Chales, Dorku, Bortei Ellen, and Aryeetey, Ernest “Global Financial Crisis Discussion Series: Ghana”, May 2009, Overseas Development Institute 111 Westminster Bridge Road

- IMF, “Regional Economic Outlook Sub Sahara Africa“, April 2009,

- Otoo, Kwabena Nyarko, and Adjaye, Prince Asafu “The effects of the Global economic and Financial crisis on the Ghanian economy and Labour Market”, Labour Research and Policy institute November, 2009

- Paulo, Drummond and Gustavo Ramirez “Spillovers from the rest of the World into Sub Sahara Countries”, IMF working paper 2009

- World Bank “Africa’s Paulse: An analyses of trends shaping Africa Economic feature” April 2010

- World Bank “Overview of South Africa’s economy”

- IMF “Regional Economic Outlook, Sub-Shara Africa; Staying the course ”October 2014

- N’zue, Felix Fofana “Impact of the Global Financial Crisis on Trade and Economic Policy Making in Africa” African center for economic transformation, 5th GTA report

- OECD “Economic Surveys: South Africa 2010”

- International Trade Center “Data and Statistics”