ESHA SAHA

INTRODUCTION:

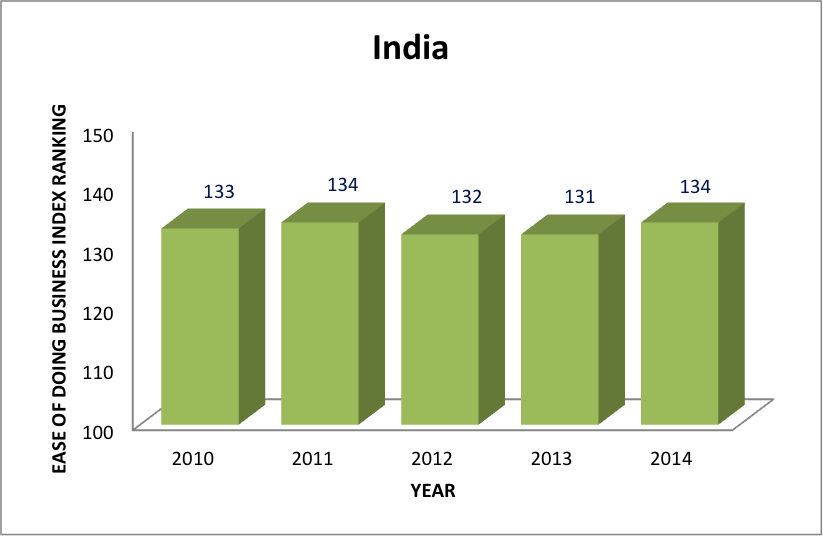

In the ‘Ease of Doing Business’ ranking of 189 countries, India has dropped from the 131st rank last year to 134thin 2014.The very fact that it is easier to do business in Nepal (105), Bangladesh (130),Pakistan (110) than in India, and that India is getting to be a tougher place to do business, is alarming. For a country that claims to be a superpower by 2030, India performs abysmally low on various ‘Ease of Doing Business’ parameters such as starting a business, dealing with construction permits, getting electricity, registering property, paying taxes, trading across border, enforcing contracts or resolving insolvency. However, in this paper, I have analyzed the following four sectors: 1.Starting of business, 2. Enforcement of contracts, 3.Infrastructure (concentrating on roads and highways sector) 4.Tax structure. In each sector certain policy measures have been suggested to improve the process of starting up and doing business across the country.

In the ‘Ease of Doing Business’ ranking of 189 countries, India has dropped from the 131st rank last year to 134thin 2014.The very fact that it is easier to do business in Nepal (105), Bangladesh (130),Pakistan (110) than in India, and that India is getting to be a tougher place to do business, is alarming. For a country that claims to be a superpower by 2030, India performs abysmally low on various ‘Ease of Doing Business’ parameters such as starting a business, dealing with construction permits, getting electricity, registering property, paying taxes, trading across border, enforcing contracts or resolving insolvency. However, in this paper, I have analyzed the following four sectors: 1.Starting of business, 2. Enforcement of contracts, 3.Infrastructure (concentrating on roads and highways sector) 4.Tax structure. In each sector certain policy measures have been suggested to improve the process of starting up and doing business across the country.

1. STARTING A BUSINESS

Innumerous entry level barriers act as major impediment in starting a business in India. There are 12 procedures involved in starting a business in India, beginning from obtaining Director Identification Number (DIN)to registering for employee’s provident fund and medical insurance. The procedure for registering a company in India takes 27 days, costing 47.3% of per capita income. The minimum paid up capital for Private and Public Limited Company in India is Rs.1, 00,000/ Rs.5, 00,000 respectively which is the highest in the South Asian Region. When compared with other South Asian countries, India lags well behind in terms of starting a business. Even though China has more procedures (13) than India (12), it must be noted that the cost of these procedures is just 2% of per capita income. On the other hand, start ups in Australia require 3 procedures and take 2.5 days, costing just 0.7% of the per capita income. Even a country like Indonesia does better than India in terms of number of procedures (10), per capita cost (20.5) and minimum paid in capital (38.5). According to World Bank report on “Doing Business 2014: India”, the government of India since 2009 has failed to introduce any significant regulatory reforms in the sector apart from establishing an online VAT registration system in 2011 and replacing the physical stamp previously required with an online version. India has only partially succeeded in reducing the administrative burden of paying taxes by abolishing the fringe benefit tax.

Exhibit 1: Start of doing business ranking of BRIC counties

India’s poor ranking in this parameter can be attributed to failure of Indian States to establish a one stop shop for application, procurement and clearance of various licenses. For e.g. in order to start a business one must procure multitude of clearances and licenses such as industrial license, compulsory license, environmental clearance license, factory license , shops and establishment license, import license, export license and central exercise license, trade license and various other types of licenses depending upon the nature of business etc. Thus, absence of one time shop has exacerbated the problems of entrepreneurs who often get caught up in red tape, lengthy investment and business approval processes.

However, in 2013, Department of Industrial Policy and Promotion (DIPP) in collaboration with Infosys launched eBiz project. The project intends to provide online single stop shop for all business licenses, clearances, approvals, no objection certificates, permits and even filing of returns so as to prevent the entrepreneurs running from department to department filing forms and procuring clearances. The first phase of the project was piloted in Andhra Pradesh, Delhi, Haryana, Maharashtra and Tamil Nadu. While the portal in its first phase only provided information on forms and procedure, the second phase of the project launched in 2014 has added two more services such as industrial licenses and industrial entrepreneur’s memorandum along with setting up of payment gateway by the Central Bank of India.

This ambitious project, if implemented successfully, can go a long way in easing the process of starting business in India. It must be noted that online approval and issuance of both Central and State level clearances in a time bound manner would be necessary for successful implementation of this project. Another impediment to the implementation of this project is the likely resistance of those departments that are used to running their services manually or in the offline. Under the UPA government, the project faced a stiff opposition from Ministry of Environment and forests, the Central Board of Excise and Customs and the Central Board of Direct Taxes. The reluctance of various departments to change their modus operandi via digitization of their services has started to cast a cloud over the success of this project. It has now become essential for the Ministry of Commerce and Industry to actively promote the project at all State and local levels so as to help India gain a competitive edge in the commercial and industrial market. In addition to this, India’s federal structure characterized by power sharing between States and the Center and decentralized decision making process has attributed to the problem of varying business and economic conditions across India’s 29 States and 7 Union territories. Thus, the Central government must undertake consensus building measures to ensure that major policies formulated at the Center gets implemented in pith and substance across various States.

2.ENFORCEMENT OF CONTRACTS

With regard to enforcement of contracts, India performs abysmally, ranking 186th out of 188 countries that were surveyed by the World Bank and International Financial Corporation. The Doing Business report notes that there are 46 procedures to be undertaken to enforce a contract in India, the time taken to enforce a contract is 1,420 days and the cost of enforcement of a contract is a whopping 39.6% of the claim which significantly undermines the rationality of pursuing judicial recourses. The length of the time taken by Courts to decide cases combined with exorbitant litigation costs has encouraged firms to resolve disputes informally. The World Bank has repeatedly recommended that rules of civil procedure should be amended to restrict the number of adjournments judges can give and that judges must be allowed to impose strict time limits on the parties.

Many countries such as Poland have made progress in enforcing contracts by introducing commercial courts of first instance and implementing e-filing system. It is to be noted that specialized commercial court system leads to greater specialization of judges- resulting in faster resolution, cheaper contract enforcement, shorter court backlogs and increased efficiency. Thus, India must seek to establish commercial division in High Courts to cater exclusively to commercial disputes above a certain threshold value. India should also consider implementation of electronic court case management system that monitors and manages cases on court dockets from the filing of claims until judgments are issued, which may lead to lower costs and faster disposal of disputes. For example, instead of physical delivery of court notice to the defendant, the court may provide defendant notification service via email, SMS or telephone contact, this will significantly reduce the period between filing of the case by the plaintiff and the first hearing of the case. Thus, proliferation of Commercial courts of first instance combined with E-filing, electronic case management system, amendment to Civil Procedure Code to limit the number of adjournments per case and disposal of cases in time bound manner can go a long way in improving the business environment of this country.

2.1 Lack of effective Alternative Dispute Resolution mechanism (ADR):

Most commercial agreements invoke arbitration clause to seek quick and cost effective settlement of disputes but in India, the Arbitration and Conciliation Act 1996 has failed to address disputes in such manner. The Act is weak with regard to enforceability of awards granted by Arbitrators and it has been observed that almost all awards are appealed against, resulting in long drawn disputes that often last 3 to 10 years.

Alternate Dispute Resolution (ADR) in India has failed to expedite the process of disposal and enforcement of contracts. Many commercial lawyers have argued that failure to develop Arbitration as quick and cost effective mechanism for resolution of commercial disputes can be directly attributed to appointment of retired judges as arbitrators. According to them, retired judges often fail to shed the trappings of “litigation mindset” which makes the whole procedure formal, adversarial, expensive and inflexible. In addition to this, astronomical fee charged by the judges (which is sometimes as high as Rs 18 lakh per sitting) has further eroded the faith of companies in Alternative dispute resolution mechanism. The situation is quite different elsewhere. In fact, in the panels of arbitrators who may be selected by those having disputes, maintained by the American Arbitration Association, lawyers dominate in commercial fields of arbitration, college professors make up the second largest group of arbitrators, while physicians, dentists, accountants, managers and other professionals form the third largest group of arbitrators.

It is equally important to amend Section 34 of The Arbitration and the Conciliation Act 1996, under which the Arbitration award can be challenged in the court. There is an urgent need to “nullify” the decision of the Indian Supreme Court in ONGC v Saw Pipes (2003) [http://indiankanoon.org/doc/919241/] in which the court held that an award could be set aside on grounds of “public policy” if it is contrary to Indian law. The broad implication of the term “public policy” has exposed all awards to be questioned in courts and has made commercial dispute resolution a time consuming and expensive process.

In fact, United Kingdom mandates that arbitral awards can be challenged only on the following three grounds:

1. Lack of substantive jurisdiction of the Arbitration Tribunal.

2. Serious irregularity affecting the Tribunal or proceedings.

3. Error of law arising out of an award made in the proceedings.

Reforms in the Arbitration Act (AA) are necessary to create a positive business climate in the country. Such reforms will expedite the process of disposal of commercial disputes in an effective manner.

3.INFRASTRUCTURE: Highways/Road Sector

While the Prime Minister of the country has persistently asserted that development of infrastructure is essential for economic growth, the private players in the country plagued by time and cost overruns of these projects have become increasingly wary of making heavy investments in this sector. It is estimated overall that the infrastructure sector will require investment of $1 trillion out of which the government expects that 50% of the expenditure would be borne by private players through Public Private Partnerships.

It is to be noticed that in the roads sector, the National Highway of India authority was recently forced to replace build–operate- transfer (PPP) model with the old EP&C model i.e. Engineering, Procurement and Construction model as there were hardly any bidders for road building projects on Build-Operate-Transfer (BOT) toll basis. Under an EPC contract, the government funds the construction and the road developer only has to develop the project in a stipulated period of time as opposed to BOT model under which the concessionaire undertakes the entire responsibility of financing the project and recoups it either through tolling rights or annuity. EP & C model imposes a heavy financial burden on the government and is often reflective of poor market health. This shift from BOT to EPC must be viewed in the context of delay in previous projects and mounting debt pile of India’s biggest road infrastructure companies owing to low traffic and related costs of development. In 2011-12, NHAI had awarded a record 51 projects covering 6,700 km, of which 27 were awarded to developers on premium instead of the general practice of seeking a capital grant from the Center known as Viability Gap funding.

It is to be noted that quoting a premium for a project amounts to committing an annual payment to the government over a period of the concession. Companies resort to offering a premium if they are confident that toll revenues from the project will be able to offset their project cost. However, 2012-end, the developers of Kishangarh-Udaipur-Ahmedabad and Shivpuri-Dewas road projects sent “termination notices”to the government on the ground of delay in regulatory approvals and 25 percent increase in the cost of material required for building roads since the time the projects were awarded. While the government is responsible for present situation, Companies too can be blamed for compromising on return on Equity by shamelessly indulging in aggressive bidding without performing their due diligence.

Exhibit 4 suggests that number of bidders for projects was highest in 2011-12 and lowest in 2012.

Exhibit 5: Nearly 32 Bidders bid at premium and only 13 of them opted for viability Gap funding.

One of the major causes of delay in infrastructure projects is tendering of the project by the government without completing the process of land acquisition. In India, sometimes projects are awarded when only 30% of the land has been physically acquired leading to subsequent delays in the projects. Although Land Acquisition Bill of 2013 has streamlined the process of acquisition, it does not address the question of premature tendering and inordinate delay in approvals from various sectors such as the External Finance Committee, Public Investment Board, by the Cabinet Committee for Economic Affairs, Ministry of Environment and Forest etc. There are as many as fifty approvals that are required at pre-tendering stage and lack of defined timelines for such approvals may indefinitely delay the project.

Therefore, it should become mandatory for the government to acquire at least 90 percent of land before tendering PPP and EP& C projects. To ease the process of acquisition, approvals must be given in a time bound manner and individuals must be held personally accountable for any such delay. Secondly, the government must appoint high power committee known as Performance Review Committee as proposed by planning commission, to regulate and unlock inter-ministerial deadlocks. It must monitor project portfolio, nodal agency performance and ensure transparency in performance. Such committee should have the power to summon representatives of various sectors to seek update on the status of pending approvals or clearances and act as an interface between private companies and the government.

Besides this, another factor that has led to stalling of infrastructure projects is lack of quality risk assessment skills. For example: in the national highways sub-sector, factors such as failure to identify that a particular project has been planned beyond scope or that the concerned project is based on dated cost estimate which has resulted in insufficient viability funding and failure to challenge self-defeating contractual terms such as termination of concession when traffic crosses a threshold level has been significantly responsible for cost overruns. Therefore, developers will need to improve their risk assessment and management capabilities. This would include setting up an independent group to assess and manage risks at multiple stages and developing sophisticated tools and systems to do so. The current crisis in the infrastructure sector can also be attributed to lack of a value engineering mindset as well as poor capabilities. Therefore, technical consultants should be appointed on quality-cum-cost based approach and their selection must be based on their experience and expertise.

The private sector is finding it difficult to raise funds for infrastructure owing to lack of availability of funds from the banking sector. This is because of the risk profile of infrastructure projects has increased significantly due to issues related to land acquisition, increased traffic risks, changes in the scope of projects, cost overruns etc. As a result the Government of India in 2013 has set up India’s first Infrastructure Debt Funds (IDF) worth one billion dollars to facilitate the flow of long-term debt into infrastructure projects. In fact, former Finance Minister P. Chidambaram had suggested that IDF must mobilize resources from insurance and pension sectors as these funds are available for long-term horizon.Further, in the 2011-12 budget, the rate of withholding tax on interest payments on the borrowings of IDF was reduced from 20 per cent to five per cent with an aim to enhance resource availability for infrastructure development. It is to be seen what impact these measures have on the economy but failure to curtail red tape may render them completely ineffective.

4.TAX REFORMS: REPLACE MULTIPLE INDIRECT TAXES WITH UNIFORM TAX SYSTEM

Goods and Service Tax has been implemented in over 140 countries. Its popularity stems from the fact that it follows the method of a Value added Tax which means that at every leg of a transaction where there is value addition, the Goods and Service Tax (GST) becomes applicable. This is a complete departure from the way taxes today are levied in India. GST is classically defined as destination based consumption tax. There are two aspects of GST: one that it is ultimately paid where the consumer is and second, it is a transaction tax which means that at every leg of a transaction wherever there is value addition, GST becomes applicable.

Today most assesses are subjected to multiple indirect taxes which has rendered the entire taxation system extremely complicated often resulting in poor realization of taxes by both the State and central government. Indirect taxation system in its present form means that at a central level there is excise duty on manufacture, service tax on rendering of services, central sales tax on transaction of sale of movable goods from one state to another whereas at State level there are State level Value added tax, entry tax or octroi, entertainment tax, luxury tax etc. Under the proposed taxation system, all these state and central level taxes would be replaced by a comprehensive Dual GST to be levied concurrently by the Center (CGST) and the States (SGST). This is to say that on every transaction there will be a central and a State levy. Such a simplified uniform tax structure will completely eliminate the scope of multiple interpretations of what are “goods” and what are “services” by the tax authorities. It is to be noted that interpretative disputes over what constitute as “goods” and “services” has opened floodgate of litigation by tax authorities and tax payers. For example, in the existing regime, there is no clarity as to whether software customized or otherwise, should be taxed under VAT or Service Tax.

It is also to be noted that under GST, the entire supply chain mechanism would be overhauled. In India goods are manufactured at a few factories and from there the goods are stock transferred to various states. A typically large company would have a depot per state. This requirement of having a depot per state stems from the fact that under the present taxation system while the manufacturer in State A can avail credit for Central State Tax (CST) imposed on sale of goods to State B, the dealer in State B cannot avail credit for the same when he further sells the goods to State C. This is because credit for CST can be availed only in State A where the goods originated. Therefore, most companies stock transfer goods to their respective depots located in various states in order to necessitate a local sale of goods for which dealers would get VAT credit.

Thus, the entire supply chain mechanism in India is designed around the tax structure instead of important factors such as product flows, faster reach to market which would reduce inventory and make the supply chain cost effective. Under GST, CST would be replaced by Integrated Goods and Service Tax (IGST) which would be levied concurrently by both State and Center and since it would be a consumption based destination tax imposed on every interstate transaction, manufacturers would be able to avail credit from both State and Center on every transaction irrespective of the place of origin of goods. This will allow the manufacturing companies to establish their warehouses for distribution at select strategic locations without looking at the same as tax planning options resulting in reduction in cost of operations and inventory holding costs. Thus, under GST, logistics service providers would set up and run nodal warehouses resulting in cost and time efficiency.

However, States are opposed to implementation of GST on account of fear of loss of revenue accruing from imposition of several State level taxes. Many States don’t want GST to cover petroleum products and alcohol. According to a leading national daily ‘The Hindu’, “the former contributed Rs 1,10,875 crore in sales tax revenues in 2012-13, while excise from liquor yielded another Rs 80,000 crore or so. Bringing these under GST would mean forgoing their ‘right’ to tax these products at rates they decide upon”. However, in order to persuade States to adopt GST, the Center has finally agreed to pay compensation to States for any estimated loss of revenue. Similarly, States are not agreeing to an Integrated GST(IGST) model because it is being proposed that it would be the Center that would collect the tax and pass it on to the destination states through a central clearance mechanism. Thus, owing to lack of trust and consensus building between the Center and State governments, this major tax reformation has still not seen the light of day. Unless and until tax structure is simplified, businesses in India will continue to suffer because of multiplicity of taxes rendering products uncompetitive.

CONCLUSION

In my opinion, lack of uniform economic conditions, lengthy processes of approvals, delay in introduction of major reforms and other unnecessary bureaucratic hurdles have adversely affected the business climate of our country. It is very important that the central government takes all stakeholders including various state governments into confidence before implementing policy measures that are pertinent for the improvement of the business environment in the country.

BIBLIOGRAPHY

8. PTI, 2013, FIIs to pay only 5% withholding tax on interest income, 21stMay, viewed : 16th February,2014

Director Identification Number (DIN) is a unique identification number for an existing director or a person intending to become the director of a company.

In the ‘Ease of Doing Business’ ranking of 189 countries, India has dropped from the 131st rank last year to 134thin 2014.The very fact that it is easier to do business in Nepal (105), Bangladesh (130),Pakistan (110)[1] than in India, and that India is getting to be a tougher place to do business, is alarming. For a country that claims to be a superpower by 2030, India performs abysmally low on various ‘Ease of Doing Business’ parameters such as starting a business, dealing with construction permits, getting electricity, registering property, paying taxes, trading across border, enforcing contracts or resolving insolvency. However, in this paper, I have analyzed the following four sectors: 1.Starting of business, 2. Enforcement of contracts, 3.Infrastructure (concentrating on roads and highways sector) 4.Tax structure. In each sector certain policy measures have been suggested to improve the process of starting up and doing business across the country.

In the ‘Ease of Doing Business’ ranking of 189 countries, India has dropped from the 131st rank last year to 134thin 2014.The very fact that it is easier to do business in Nepal (105), Bangladesh (130),Pakistan (110)[1] than in India, and that India is getting to be a tougher place to do business, is alarming. For a country that claims to be a superpower by 2030, India performs abysmally low on various ‘Ease of Doing Business’ parameters such as starting a business, dealing with construction permits, getting electricity, registering property, paying taxes, trading across border, enforcing contracts or resolving insolvency. However, in this paper, I have analyzed the following four sectors: 1.Starting of business, 2. Enforcement of contracts, 3.Infrastructure (concentrating on roads and highways sector) 4.Tax structure. In each sector certain policy measures have been suggested to improve the process of starting up and doing business across the country.