By : Athma Maria Mathew

Abstract

The challenges of balancing the fiscal equation within a quasi-federal country, in addition to the irregularities in featuring a mixed economy, is a rising crisis in India’s democracy. This article attempts to address these issues by evaluating the financial markets involved in constructing India’s first International Deepwater Multipurpose Seaport at Vizhinjam, Kerala. The ultimate objective of this article is to evaluate the feasibility of the project based on the credibility of its capital structure.

Introduction

The Vizhinjam International Sea Port is located in Thiruvananthapuram, Kerala. The project has completed Phase 1. Phases 2 and 3 are under development. The Concession Agreement for the Development & Operation of Vizhinjam International Deepwater Multipurpose Seaport Kerala was signed on the 17th of August 2015 between the Government of Kerala and Adani Vizhinjam Ports Private Limited. Therefore, Adani Vizhinjam Port Private Ltd. is the concessionaire for this project.

Financing Vizhinjam:

The capital structure of the seaport is a collaborative construction of the Adani group, the Kerala Government, and the Central government.

Capital Structure

| Government of Kerala | 61.5% |

| Government of India | 9.6% |

| Adani Vizhinjam Port Private Ltd | 28.9% |

While there is no official approximation as of 2024, considering the capital intensity involved in the infrastructure project, the debt-equity ratio being greater than 1%, calculated below on the basis of the 2022 Annual Report, need not necessarily be a matter of concern. Debt to

Equity ratio = Total Debt/ Total Equity

Debt to Equity ratio = 7,71,25,53.098/3,79,88,04,451 = 2.03%

Adani ports in general have a consolidated debt-to-equity ratio of 1.04% and a standalone ratio of 1.67%. However, the factuality behind the figures can be better demonstrated through understanding the circumstances surrounding the projected capital structure.

State of Kerala v. Union of India, 2024. SC 476.

The financial year of 2024-2025, has pushed the State of Kerala into financial agony. The government has mismanaged its finances, creating a debt-stressed environment of fiscal deficit. State of Kerala v. Union of India further displays complications in the financial stability of the state. The Government of Kerala was demanding the Central Government to enable the state to borrow ₹26,226 crores on an immediate basis as an interim relief, while the Central Government was reluctant to sanction the amount, citing the State’s excess borrowings and that more loans would pose a threat to the fiscal security of the nation.

The plaintiff, Kerala, cited the below data in its defence (Fig.1.1), claiming that its fiscal deficit was showing a positive trend thereby establishing an eligible fiscal space to borrow. However, the counsel for the Union argued that the narrowing fiscal deficit was a planned adjustment to compensate for the over-borrowings of 2020-2021, 2021-2022, and 2022-23. This brings us back to ground zero, where we conclude that Kerala is incapable of accessing borrowing benefits; even the Court reached a similar conclusion, denying Kerala the prayed interim relief as it was unable to prove the underutilised fiscal space for additional borrowings.

Figure 1.1

Despite this refusal for interim relief, the case was settled for ₹13, 608 crores in order to lay off the debt burdens of the Government of Kerala. But this fund allocation was for the benefit of the pending dues of the state such as pension funds, dearness allowance, subsidies, and other budgetary obligations. The state’s incompetency in funding any macro-level public-private partnership project like that of Vizhinjam International Seaport could not be clearer.

Perhaps this financial crisis is a factor contributing to the delay in the progress of the infrastructure development. On 15 February, the Centre, the State, and Adani Vizhinjam Port Pvt. Ltd (AVPPL) entered into a tripartite agreement for the viability gap fund of ₹817.80 Cr from the central government. The VGF is capped at 40% of the total project cost of ₹4089 crores. They also made a second agreement on premium sharing whereby, the Centre receives a 20% share of the revenue from the port from 2034. However, on 9 April 2025, the State and Centre entered a MoU which changed the VGF status from a grant to a loan. This broadening budget of the Vizhinjam project is merely reflective of the financial strains of the State.

Another challenge that we must acknowledge is the Budget allocation for 2024. Budget 2024, from a wider angle, was similar to (a + b)2 = a2 + 2ab + b2, 2ab, the focus, being Andhra Pradesh and Bihar. Despite the wailing conditions of Kerala’s economy, the budget allocation for Kerala was not supportive. Kerala was expecting ₹24,000 crore as a special economic package to stabilise the economy and ₹5,000 crore as special assistance for the Vizhinjam seaport project. But both the demands remain unsatisfied.

These elements cast some doubt on the accuracy of the anticipated debt-equity ratio; the fiscal deficit and the resultant change in the capital structure have a profound impact. As the capital intensity increases, the need for debt automatically increases, demolishing every possibility of reviving Kerala’s economy. Looking prospectively, fluctuations in prevalent interest rates could also damage the financial security of the project.

The Hindenburg report on the Adani Group contradicted the publicly claimed and released financial sustainability of the project; it claims that the publicly available data is deceivingly exaggerated.

Figure 2.1 elucidates the enigmatic rise of stock prices over the past 3 years. “Both Adani Enterprises and Adani Ports feature in India’s Nifty 50 Index”. The report suggests that this sudden variation in the Stock % of Gain is logically impossible as the face value of the company shows that 7 listed companies run an 85% disadvantage. Even though the figures concerning the Adani ports remain substantiated, the rest signify exaggeration that reflects the incompetency of the corporate entity to fund the infrastructural project.

Here, the 85% disadvantage refers to the overvaluation experienced by the 7 listed Adani companies. The report states that it is unusual for infrastructural firms to show trends similar to high-growth tech companies because they have relatively low growth and low multiplicity of enterprises. The data given in Figure 2.2 show 85%+ downside when compared to other industries in the market.

Except for Adani Wilmar and Adani Ports, the debt-equity ratio of the rest of the entities is less than 1.0, indicating short-term liquidity. Concerning unrestricted cash, Adani Port in particular is the only listed entity that has the potential to generate positive cash flow and maintain a reserve of INR 86 billion.

However, the Hindenburg report fails to recognize that the stocks of the Adani Group are interconnected and that the presence of features like cross-holdings and inter-company loans could pose a significant risk to sustainable stock growth, and recent projects like the Vizhinjam International Sea Port in the long run.

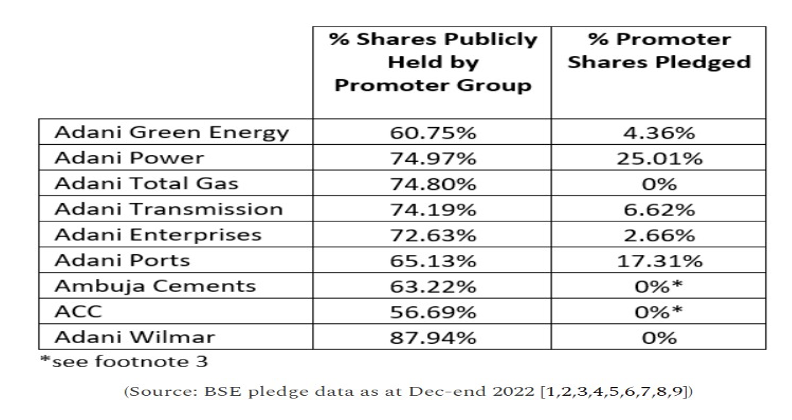

As per the Report, huge portions of promoters’ equity are pledged as collaterals for loans by Adani insiders and KMP; essentially, on default of the share prices by these personnel, the lender may forcefully liquidate these shares.

However, the intricacy of interconnected shareholding patterns between individual entities of the Group, given in Figure 2.3, proves beyond doubt the possibility of an under-development project like the Vizhinjam Sea Port becoming a sham.

Conclusion

This analysis projects the underrated transition of Indian markets and their federalism, i.e., the former towards capitalism and the latter towards unitary control. The democracy of this nation is compromised under the undue influence of private actors. Our financial markets lack inclusivity in terms of development but they reflect deeply in taxing the ordinary citizens to share debts. These hybrid models of development pull all the stakeholders together when one of them is at risk.

About the Author: Athma Maria Mathew is an undergrad at O.P. Jindal Global University pursuing her BA (Hons.) in Legal Studies. She finds her solicitude in socio-economic justice and is deeply interested in Commercial and Administrative Law within the context of the Indian Constitution.